Who’s Buying the Long End?

Decoding the Quiet Survival of 30-Year Treasuries

The Long Bond as the Strategic Bridge to a New System

In an increasingly complex financial world shaped by structural deficits, shifting geopolitical alliances, and the rapid evolution of digital infrastructure, the long-dated U.S. Treasury bond continues to play a role far more important than its recent price action suggests.

Although long-end instruments such as TLT and ZB (30-year Futures) have exhibited notable weakness, institutional demand for 30-year bonds has remained steady. This quiet but persistent support is not the result of bullish sentiment, but rather the outcome of strategic necessity.

The long bond remains deeply embedded in the global financial system. From regulatory capital requirements to collateral frameworks and sovereign liquidity needs, its function extends beyond yield generation.

It serves as a linchpin for market stability.

To abandon it too soon would risk structural collapse at a time when the architecture for the next system is not yet fully constructed. This is why Treasury auctions have continued to clear with consistency. Despite broader market dislocations, indirect bidders such as foreign central banks, sovereign wealth funds, and insurance portfolios have continued to anchor demand.

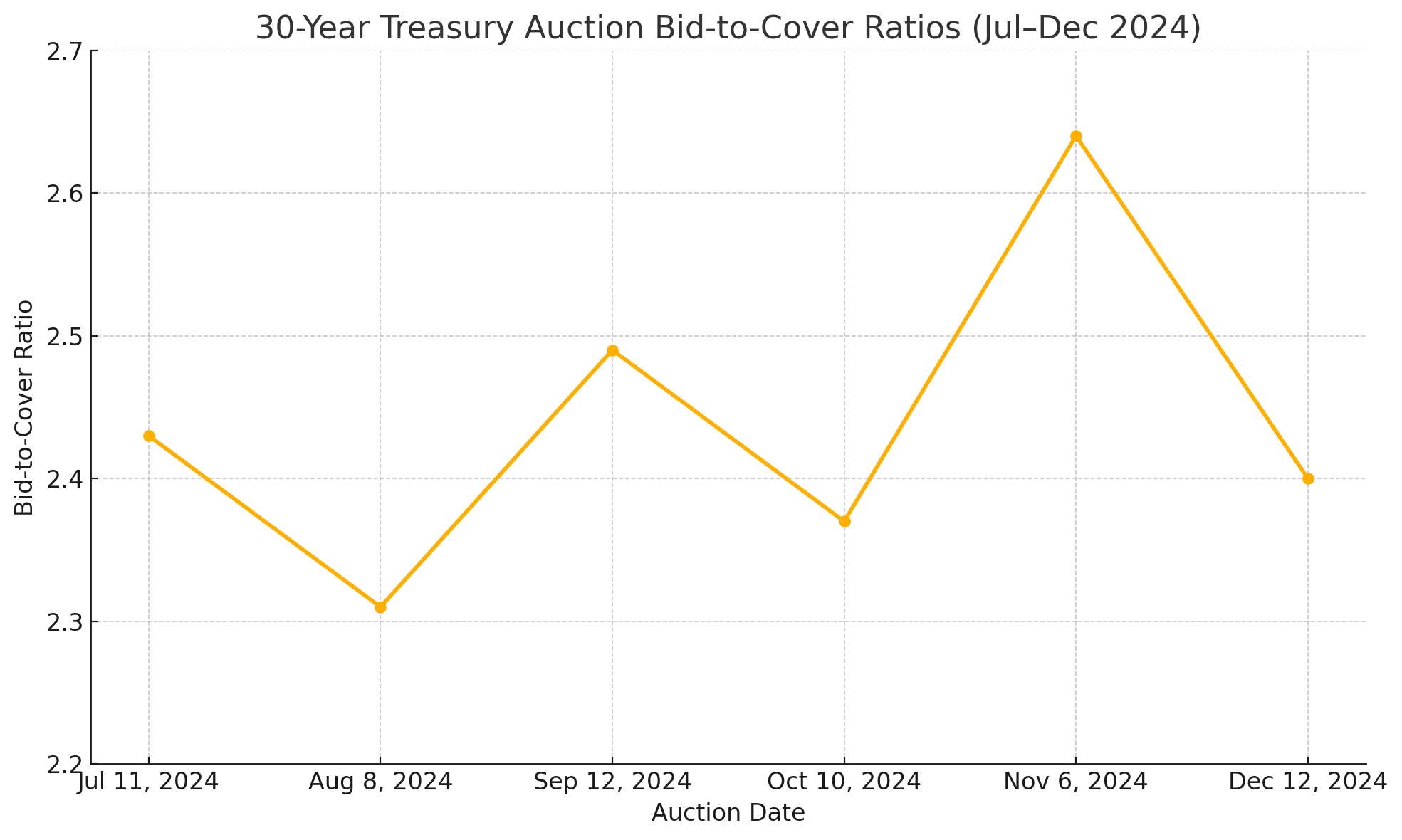

The June 2025 30-year bond auction posted a bid-to-cover ratio of 2.43. While not an outlier, this figure sits above the ten-auction average and suggests that demand, while not explosive, remains consistently solid.

For readers unfamiliar with this metric, the bid-to-cover ratio reflects the volume of bids relative to the bonds available for sale. A ratio above 2.0 suggests that demand comfortably exceeded supply, a signal that investors were more than willing to absorb the offering.

More revealing is the fact that primary dealers were allocated just 11.4% of the issuance. These dealers typically serve as the backstop for auctions, absorbing unsold bonds and distributing them through the financial system. The unusually small share awarded to dealers implies that the lion’s share of demand came from indirect bidders.

This is a period in which the long bond is no longer viewed as a safe haven destination, but rather as a bridge, serving as a strategic instrument used to preserve systemic coherence while the foundations of a new financial infrastructure are quietly being assembled.

Below, we articulate why we believe we are in the midst of a historic transitional phase.

Keep reading with a 7-day free trial

Subscribe to AXELWORKS to keep reading this post and get 7 days of free access to the full post archives.